How to Pay Less Tax by Splitting Income

Learn how to pay less tax by splitting income. Discover effective tax strategies, including spouse income splitting, family trusts, and dividend splitting, to reduce your overall tax burden and maximize savings.

8/22/20253 min read

If you’re looking to lower your tax bill, one strategy that can be highly effective is income splitting. This method involves distributing your income among different family members or legal entities to reduce the total taxable amount. By spreading income across multiple people, you can take advantage of lower tax brackets, tax credits, and deductions that may not be available to a single individual.

In this post, we’ll explore how income splitting works, its benefits, and key considerations to help you pay less tax.

What is Income Splitting?

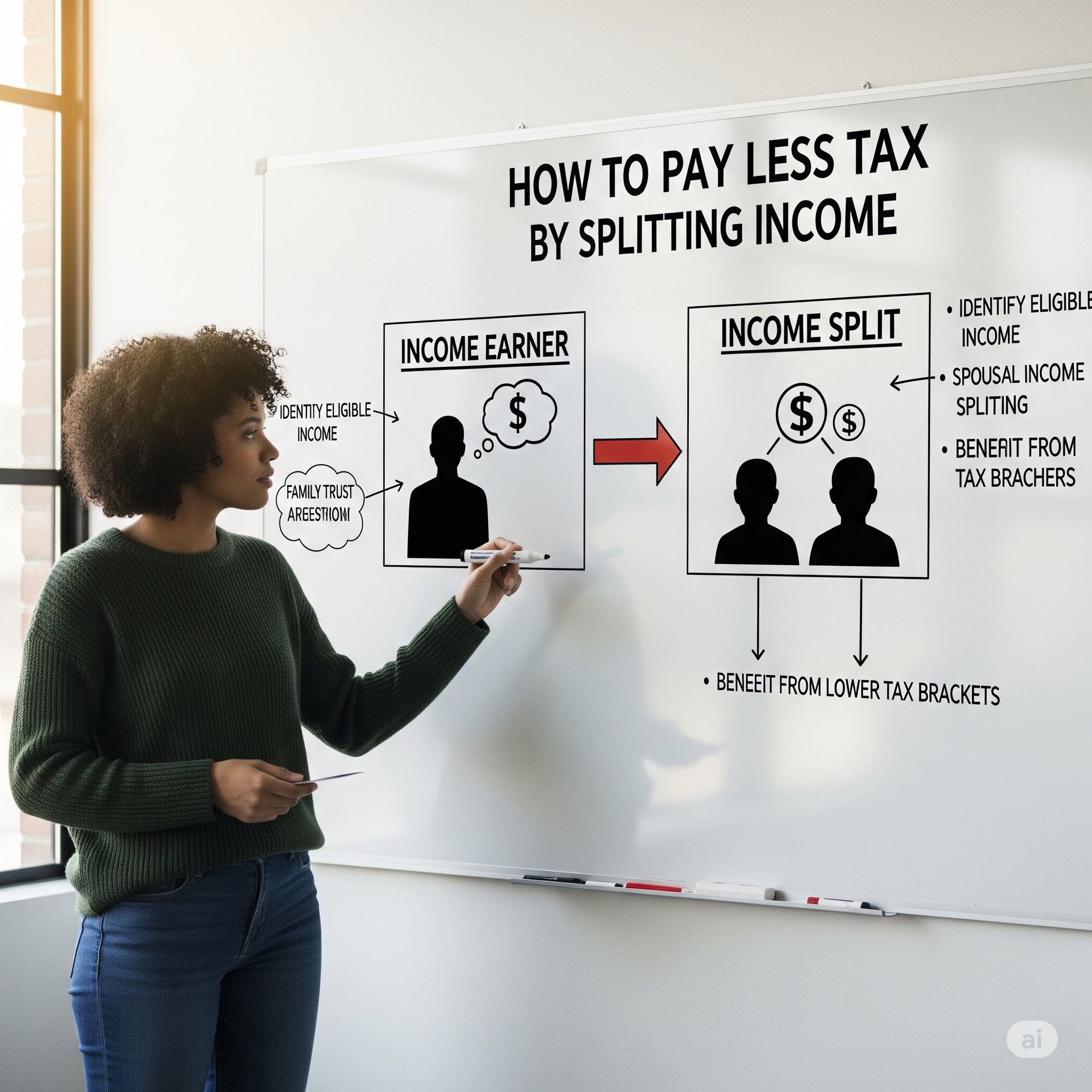

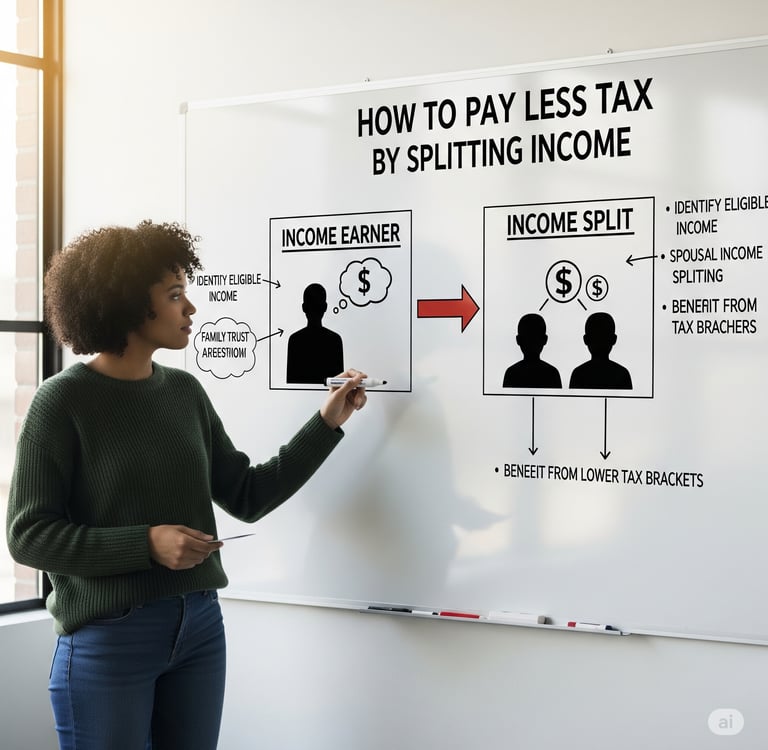

Income splitting is a tax strategy that involves distributing income from a higher-income earner to family members who have lower incomes. The goal is to lower the overall tax burden by reducing the amount of income taxed at the higher rate. Income splitting can be done through various means, including gifting assets or using trusts.

How Does Income Splitting Work?

The process of income splitting typically works in the following ways:

Spouse Income Splitting: If you and your spouse are in different tax brackets, you can transfer income or assets to your spouse to reduce your combined taxable income. This can be achieved through joint accounts, loans, or other legal structures.

Family Trusts: A family trust allows you to distribute income to beneficiaries (family members, for example) who are taxed at lower rates. This strategy is particularly effective for families with significant wealth or business interests.

Dividend Splitting: If you own a business, you can split dividends among family members or partners who are in lower tax brackets. This allows you to reduce the total tax burden on the business’s profits.

Gifting Assets: Gifting assets to family members in lower tax brackets can also be a way to reduce taxable income. For example, gifting shares or properties can result in lower overall taxation when the assets generate income or appreciate in value.

Benefits of Income Splitting

Lower Tax Brackets: By distributing income, you can take advantage of tax brackets that may be lower for family members or other entities. This can lead to significant savings.

Access to Tax Credits: Certain family members or dependents may be eligible for tax credits that would not otherwise apply. By splitting income, you can maximize available credits and deductions.

Increased Financial Flexibility: Income splitting can also create financial flexibility, allowing family members to invest or save more without the burden of high taxes.

Effective for Retirement Planning: Income splitting can be part of a retirement strategy, where income is split between younger family members who have lower earning potential. This can allow for more efficient wealth accumulation.

Key Considerations

While income splitting can be an effective way to lower taxes, there are a few important considerations:

Legal Restrictions: Tax laws vary by jurisdiction, and some countries have anti-avoidance rules that limit the ability to split income. It’s essential to consult with a tax advisor to ensure compliance with local tax regulations.

Complexity of Setup: Income splitting strategies, such as trusts or joint accounts, may require careful planning and legal setup. It’s important to have a clear understanding of how these structures work to avoid unintended tax consequences.

Gift Tax Implications: Depending on the size and type of gifts made, you may incur gift tax obligations. Make sure to understand any tax liabilities that could arise from transferring assets.

Conclusion

Income splitting can be a powerful tool to reduce your tax liability. By strategically distributing income among family members or legal entities, you can lower your overall tax burden and take advantage of tax-saving opportunities. However, it's essential to understand the rules and regulations surrounding income splitting to ensure that you're using it effectively and legally. Always consult a tax professional before implementing any income splitting strategies to make sure you're making the best decision for your financial situation.

If you’re looking to optimize your taxes, don’t hesitate to contact the experts at TIKI TAX to explore your options further.

TiKi Tax

© 2025. All rights reserved.