How to Pay Yourself the Smart Way (Draw vs. Salary)

Should you pay yourself a salary or take an owner’s draw? Learn the smart way to pay yourself as a small business owner in Canada — and how it affects your taxes, CPP, and cash flow.

10/17/20252 min read

Paying Yourself as a Business Owner

One of the most common questions small business owners in Canada ask is:

“How do I pay myself — salary or draw?”

Whether you run an incorporated business or operate as a sole proprietor, how you pay yourself affects taxes, CPP, and financial planning. Let’s break down both methods so you can choose what’s best for you.

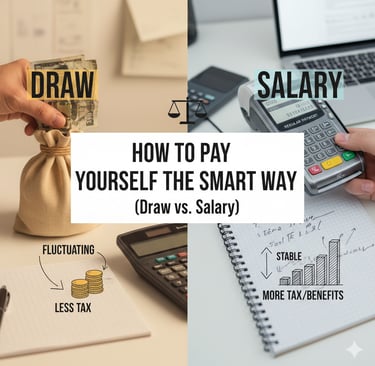

1. What Is an Owner’s Draw?

If you’re a sole proprietor or in a partnership, an owner’s draw means you take money directly from your business profits for personal use.

It’s not considered a salary — you’re simply withdrawing from the business account.

Key points to know:

You don’t pay yourself “wages.”

You’re taxed on your net business income, not the money you draw.

You don’t pay CPP (Canada Pension Plan) through payroll, but you pay both the employer and employee portions when filing taxes.

This option gives you flexibility — you can take money out anytime. But it requires discipline to set aside enough for taxes and CPP at year-end.

2. What Is a Salary (Payroll Method)?

If your business is incorporated, you can pay yourself a salary just like an employee.

That means:

You set up payroll and issue regular paycheques.

The business withholds income tax, CPP, and EI (if applicable).

You report the income on a T4 slip at tax time.

A salary helps you build CPP contributions, qualify for RRSP room, and show consistent income — which can be useful for getting loans or mortgages.

However, it also means extra paperwork and payroll costs.

3. Tax Differences Between Draw and Salary

The main difference comes down to when and how you pay tax.

With a draw, tax is calculated on your business’s total profit at year-end.

With a salary, the business deducts payroll taxes throughout the year — just like any regular employee.

Incorporated owners can also split income between salary and dividends to balance taxes and cash flow. This is where professional tax planning really pays off.

4. Which Option Is Better for You?

There’s no one-size-fits-all answer — it depends on your business structure and income level.

If you’re a sole proprietor, a draw is simpler and more flexible.

If you’re incorporated, a salary offers more structure and long-term benefits (like CPP and RRSP).

Many business owners use a mix of both to balance cash flow and minimize taxes.

Here’s a simple rule of thumb:

Need consistency? Go with a salary.

Want flexibility? Choose a draw.

Want the best of both? Combine them strategically.

5. The Smart Approach: Plan Ahead

The smartest way to pay yourself is to plan your compensation before tax season.

A tax advisor can help you:

Estimate your annual income

Decide how much to pay yourself

Structure payments to minimize taxes

Ensure compliance with CRA payroll and reporting rules

This approach keeps your business cash flow healthy and prevents tax surprises later.

✅ Final Thoughts

Whether you take an owner’s draw or pay yourself a salary, the key is understanding how each method impacts your taxes, benefits, and business finances.

If you want a clear, tax-efficient strategy tailored to your situation, the team at Tiki Tax can help you find the balance that works best — so you can pay yourself the smart way.

TiKi Tax

© 2025. All rights reserved.