Should You Consolidate Your Debt? Pros & Cons

Considering debt consolidation? Learn the pros, cons, and key factors to decide whether consolidating your debt is the right financial move for you.

12/4/20252 min read

Managing multiple debts can feel overwhelming—especially when each loan comes with different due dates, interest rates, and payment terms. Debt consolidation is a popular strategy that helps simplify your finances by combining multiple debts into a single loan. But is it always the right choice?

In this article, we break down the pros and cons of debt consolidation, when it makes sense, and when you might want to explore other options.

What Is Debt Consolidation?

Debt consolidation is the process of merging multiple debts—such as credit cards, personal loans, or payday loans—into one new loan with a single monthly payment. Ideally, this new loan offers:

A lower interest rate

A longer repayment period

Easier financial management

Common methods include personal loans, balance transfer credit cards, or home equity loans.

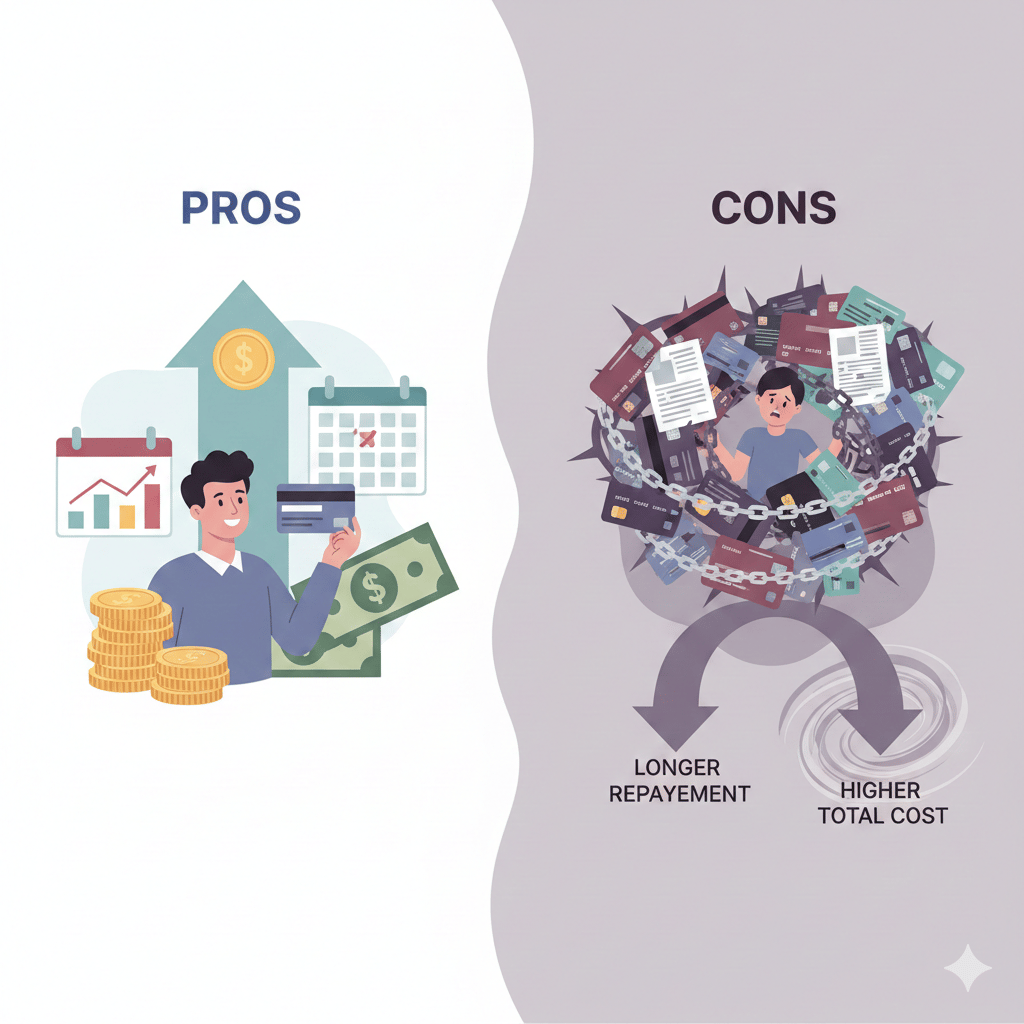

The Pros of Debt Consolidation

1. One Simple Monthly Payment

Instead of juggling several due dates and bills, debt consolidation simplifies everything into one predictable payment. This reduces stress and lowers the risk of missed payments.

2. Potentially Lower Interest Rates

If your current debts have high interest rates—especially credit cards—you may qualify for a consolidation loan with a lower rate, helping you save money long-term.

3. Improved Cash Flow

Lower interest or longer repayment terms can reduce your monthly payments, giving you more breathing room in your budget.

4. Faster Debt Repayment

Some consolidation plans are structured to help you pay off debt sooner by focusing on a clear repayment schedule.

5. Can Improve Your Credit Score

Over time, making on-time payments on your new consolidation loan can boost your credit score and show healthy debt management.

The Cons of Debt Consolidation

1. You May Pay More in the Long Run

If your consolidation loan extends your repayment period, your total interest paid may end up being higher—even if the monthly payment is lower.

2. Not Guaranteed Lower Interest

You typically need good credit to qualify for the best rates. If your credit score is low, the new loan might not save you money.

3. Risk of Accumulating New Debt

Many people pay off their credit cards through consolidation but then start using them again, creating a deeper cycle of debt.

4. Fees and Additional Costs

Some consolidation loans come with:

Origination fees

Balance transfer fees

Early repayment penalties

Always review terms carefully.

5. Secured Loans Put Assets at Risk

If you use a home equity loan or another secured loan, you could risk losing your home if you can’t make payments.

When Is Debt Consolidation a Good Idea?

Debt consolidation might be right for you if:

Your credit score qualifies you for a lower interest rate

You struggle to manage multiple monthly payments

You have high-interest credit card debt

You want a clear, structured repayment plan

You’re committed to not increasing your debt again

When You Should Avoid Debt Consolidation

It may not be the right solution if:

You have poor credit and won’t qualify for better rates

Your debt amount is too high to realistically pay off

You don’t have stable income to make monthly payments

You’re using consolidation to avoid addressing spending habits

In these cases, alternatives like credit counselling, debt settlement, or consumer proposals may be more appropriate.

Debt Consolidation Alternatives

If consolidation isn’t suitable, consider:

Debt Management Plans — Work with a credit counsellor to negotiate lower interest.

Debt Settlement — Negotiate with creditors to pay less than owed.

Consumer Proposals (Canada) — Legally reduce your debt through a licensed insolvency trustee.

Budgeting and Financial Coaching — Improve spending habits and create a debt payoff plan.

Final Thoughts

Debt consolidation can be a powerful tool for simplifying your finances, reducing interest costs, and helping you regain control—but it’s not a one-size-fits-all solution. Understanding the pros, cons, and your financial situation is essential before deciding.

TiKi Tax

© 2025. All rights reserved.